Did you know most Oklahoma business owners pay more for workers comp than they should?

It’s true. And the frustrating part is — it’s usually not their fault. Nobody sat down with them and explained how the price is set. So they just pay the bill every year without knowing if it’s fair.

We fix that every day at Eagle National. And we see the same five mistakes over and over again.

Here’s what they are — and how to fix each one.

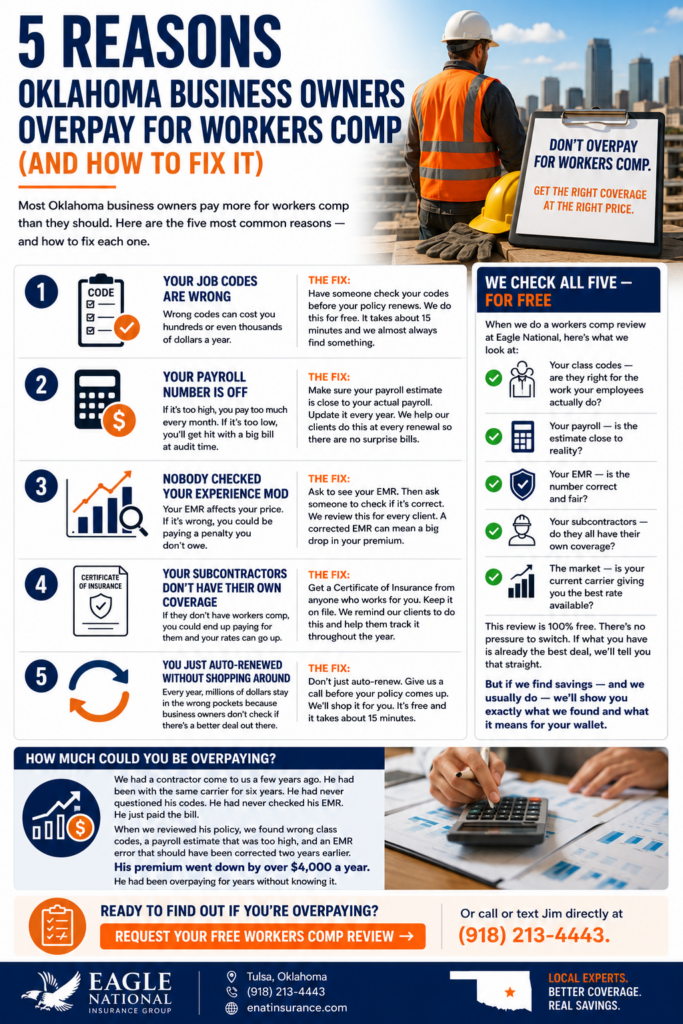

Reason #1: Your Job Codes Are Wrong

Every job gets a code number. That code tells the insurance company how risky the work is.

An office worker has a low code. A roofer has a high code. The higher the code, the more you pay.

Here’s the problem. A lot of policies have the wrong codes on them. Maybe your business changed. Maybe the codes were set wrong from the start. Either way — you’re paying the wrong price.

Wrong codes can cost you hundreds or even thousands of dollars a year.

The fix: Have someone check your codes before your policy renews. We do this for free. It takes about 15 minutes and we almost always find something.

Reason #2: Your Payroll Number Is Off

Workers comp is priced based on how much you pay your employees. The more payroll you have, the more you pay.

But here’s where it gets tricky. If your payroll estimate is too high, you’re paying too much every month. If it’s too low, you’ll get hit with a big bill at the end of the year when your policy is audited.

Both are bad.

A lot of business owners set their payroll estimate when they first got the policy — and never updated it. Their business grew or shrank, but the number stayed the same.

The fix: Make sure your payroll estimate is close to your actual payroll. Update it every year. We help our clients do this at every renewal so there are no surprise bills.

Reason #3: Nobody Checked Your Experience Mod

Your Experience Modification Rate — most people just call it the EMR or the mod — is a number that reflects your claims history.

Think of it like a grade.

If your number is below 1.0, you get a discount. Good claims history means lower prices.

If your number is above 1.0, you pay more. It’s a penalty for having more or bigger claims than average.

Here’s the problem: that number can be wrong. Errors happen. Old claims get counted when they shouldn’t. And most business owners have no idea what their number is — let alone whether it’s right.

The fix: Ask to see your EMR. Then ask someone to check if it’s correct. We review this for every client. If there’s an error, we can challenge it. A corrected EMR can mean a big drop in your premium.

Reason #4: Your Subcontractors Don’t Have Their Own Coverage

If you hire subcontractors, this one is really important.

When a subcontractor doesn’t have workers comp, your insurance company can count their payroll as your payroll. That means you pay for them. It also means your rates can go up.

A lot of business owners don’t know this until they get their audit bill. By then it’s too late.

The fix: Before anyone does work for you, get a Certificate of Insurance from them. That’s just a simple document that proves they have their own workers comp coverage. Keep it on file. We remind our clients to do this and help them track it throughout the year.

Reason #5: You Just Auto-Renewed Without Shopping Around

This is the biggest one.

Every year, millions of dollars stay in the wrong pockets because business owners just let their policy renew without checking if there’s a better deal out there.

Your current insurance company isn’t going to call you and say “hey, you could pay less somewhere else.” That’s not their job.

But it is ours.

As an independent agency, we’re not tied to any single insurance company. We work with many carriers. That means we can shop your coverage across multiple options and find the one that fits your business and your budget best.

Most of the time — when someone comes to us for the first time — we find savings.

The fix: Don’t just auto-renew. Give us a call before your policy comes up. We’ll shop it for you. It’s free and it takes about 15 minutes.

How Much Could You Be Overpaying?

It depends on your business. But here’s a real example.

We had a contractor come to us a few years ago. He had been with the same carrier for six years. He had never questioned his codes. He had never checked his EMR. He just paid the bill.

When we reviewed his policy, we found wrong class codes, a payroll estimate that was too high, and an EMR error that should have been corrected two years earlier.

His premium went down by over $4,000 a year.

He had been overpaying for years without knowing it.

We Check All Five — For Free

When we do a workers comp review at Eagle National, here’s what we look at:

✅ Your class codes — are they right for the work your employees actually do? ✅ Your payroll — is the estimate close to reality? ✅ Your EMR — is the number correct and fair? ✅ Your subcontractors — do they all have their own coverage? ✅ The market — is your current carrier giving you the best rate available?

This review is 100% free. There’s no pressure to switch. If what you have is already the best deal, we’ll tell you that straight.

But if we find savings — and we usually do — we’ll show you exactly what we found and what it means for your wallet.

Ready to find out if you’re overpaying?

👉 Request Your Free Workers Comp Review →

Or call or text Jim directly at (918) 213-4443.

Eagle National Insurance Group Tulsa, Oklahoma (918) 213-4443 enatinsurance.com

Eagle National Insurance Group is an independent insurance agency serving small businesses across Oklahoma. We specialize in workers compensation, general liability, and business owner policies.